為什么印度盛產碼農

Agriculture is at the center of Indian economy and any major change in the sector leads to a multiplier effect on the entire economy. With around 17% contribution to the Gross Domestic Product (GDP), it provides employment to more than 50% of the workforce. The largest industries of the country like sugar,textiles, food processing etc. are dependent on agriculture and the allied services for their raw materials. The major crops grown in India include paddy, wheat, pulses , edible oil and horticulture. Along with this poultry, fishery and animal husbandry are other major allied services. But despite the robust demand, attractive opportunities and policy support, the sector suffers from high price volatility , low income among farmers, skewed MSP rates and lack of credit facilities. Hence there is a need for a long term strategy to assess demand and supply and to forecast prices for crops.

一個 griculture是在印度經濟中心和行業導致對整個經濟產生乘數效應的任何重大變化。 它對國內生產總值(GDP)的貢獻約為17%,為超過50%的勞動力提供了就業機會。 該國最大的工業,如糖,紡織,食品加工等,都依賴于農業及其相關的原材料服務。 印度的主要農作物包括水稻,小麥,豆類,食用油和園藝。 除此家禽外,漁業和畜牧業也是其他主要的盟約服務。 但是,盡管需求旺盛,有吸引力的機會和政策支持,該部門仍遭受價格高波動,農民收入低,MSP利率偏高以及缺乏信貸便利的困擾。 因此,需要一種長期戰略來評估供需并預測農作物的價格。

Being a cereal-centric agriculture, the prices of paddy, wheat and pulses are of the most importance. Prices of vegetables like potato, tomato, onion also need to be closely monitored as they impact the food inflation rates in the country. Moreover the prices of 24 commodities under the MSP regime including 8 oil seeds , raw cotton, raw jute and copra are vital in deciding minimum support prices as well as deciding procurement prices for the Public Distribution System(PDS). Thus agriculture prices directly impact the income of producers and the food security of the nation.

作為以谷物為中心的農業,稻谷,小麥和豆類的價格最為重要。 土豆,西紅柿,洋蔥等蔬菜的價格也需要受到密切監控,因為它們會影響該國的食品通貨膨脹率。 此外,MSP體制下的24種商品的價格(包括8種油料,原棉,生黃麻和椰干)對于決定最低支持價格以及決定公共分配系統的采購價格至關重要。 因此,農業價格直接影響生產者的收入和國家的糧食安全。

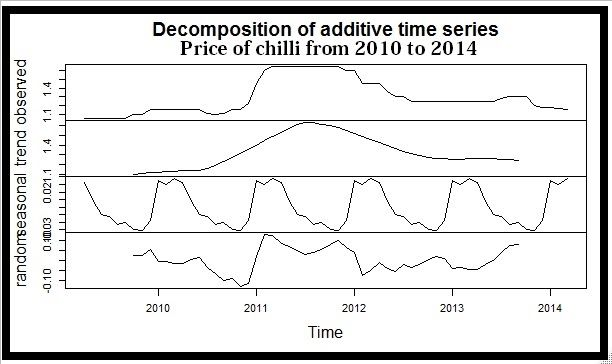

Directorate of Economics & Statistics, Agriculture (DESAg), in the Ministry of Agriculture is the prime source for agricultural statistics. Other sources include National Sample Survey Organisation(NSSO),State’s Directorate of Economics and Statistics (DES) and Central Statistical Organisation. A major part of this data is time series data, that measures agriculture prices ?over changing time frequencies — yearly, monthly, quarterly or daily. These series of prices show trends , along with seasonality and cyclic nature of agricultural prices.

農業部農業統計經濟局(DESAg)是農業統計的主要來源。 其他來源包括國家抽樣調查組織(NSSO),州經濟與統計局(DES)和中央統計組織。 此數據的主要部分是時間序列數據,該數據可以測量變化的頻率頻率上的農業價格-每年,每月,每季度或每天。 這些系列價格顯示趨勢,以及農產品價格的季節性和周期性。

These time series data associated with agricultural prices can be used for forecasting short term and long term price estimates. It can help to identify patterns and seasonal variations in prices especially with respect to production during kharif, rabi and zaid seasons. Forecasting of agricultural prices are also important for determining subsidy rates, minimum support prices, export prices etc.Thus monitoring and controlling agricultural price volatility and preplanning policies to mitigate any adverse situations. Time series of crop prices can also help to understand, interpret and explain instances of economic crisis in the agricultural sector. Intervention analysis of such time series can also provide us insights into understanding the impact of sudden price changes over other sectors and overall economy. Moreover agriculture price forecasts are essential in determining risks in agri-commodity futures and options trading markets.

這些與農產品價格相關的時間序列數據可用于預測短期和長期價格估計。 它可以幫助確定價格的模式和季節性變化,特別是在卡里夫,狂犬病和宰牲節季節的生產方面。 預測農產品價格對于確定補貼率,最低支持價格,出口價格等也很重要。因此,監測和控制農產品價格的波動性以及為減輕任何不利情況而制定的計劃政策。 作物價格的時間序列還可以幫助理解,解釋和解釋農業部門發生經濟危機的情況。 此類時間序列的干預分析還可以為我們提供洞察力,以了解突然的價格變化對其他行業和整體經濟的影響。 此外,農業價格預測對于確定農產品期貨和期權交易市場的風險至關重要。

An important component of time series data is trend and agricultural price data often show deterministic trends. Trend analysis can be performed by using ?Moving Average Method ?and ?Exponential Smoothing Method?. In the Moving Average Method, the first average is the mean of the prices in the first ?m period. The second average is the mean of the prices of ?m data points starting from the second price data up to (?m + 1) th period. Similarly, the third average is the mean of the prices of ?m data points from the third to (?m + 2) th period and so on. This new set of data is then used to determine the trend.

時間序列數據的重要組成部分是趨勢,而農產品價格數據通常顯示確定性趨勢。 趨勢分析可以使用``移動平均法''和``指數平滑法''進行。 在移動平均法中,第一個平均值是前m個時期的價格平均值。 第二個平均值是從第二個價格數據到第(m + 1)個時期開始的m個數據點的價格平均值。 同樣,第三次平均值是從第三到第(m + 2)期間的m個數據點的價格的平均值,依此類推。 然后使用這組新數據確定趨勢。

The Exponential Smoothing Method gives larger weights to recent price observations compared to past observations. Such that the weights decrease exponentially.

與過去的觀察相比,指數平滑法對最近的價格觀察給予更大的權重。 這樣權重呈指數下降。

Another component of time series, that is often present in agricultural price data is seasonality. This is evident from the fact that the harvesting of crops takes place over a certain period of time in a year and the prices fluctuate accordingly. It is thus necessary to identify the seasonality and obtain thedeseasonalized series for further model development. The methods used are the ?Dummy Variable method ?and ?Ratio to Moving Average? methods.

農業價格數據中經常出現的時間序列的另一個組成部分是季節性。 從事實來看,農作物的收獲是在一年的一定時期內發生的,價格也隨之波動。 因此,有必要確定季節并獲得反季節序列以用于進一步的模型開發。 所使用的方法是``虛擬變量''方法和``移動平均比率''方法。

Before forecasting the price of agriculture produce, it is essential to identify the presence of non-stationarity. This is necessary to avoid spurious and misleading model estimates. The most common test used for the purpose is ?Augmented Dickey Fuller(ADF) unit root test. The framework of ADF methods is based on analysis of the following model.

在預測農產品價格之前,確定非平穩狀態的存在至關重要。 這對于避免虛假和誤導的模型估計是必要的。 為此目的最常用的測試是增強Dickey Fuller(ADF)單元根測試。 ADF方法的框架基于以下模型的分析。

If the time series data is non-stationary then we make it stationary by differencing and again performing the ADF test. This step is repeated until we get a stationary time series. After getting a deseasonalized stationary series without having a deterministic trend, we can proceed to identification of the model. The model can be either ?AR(p) / MA(q) / ARMA(p,q)?. To determine the model and its order we calculate the sample ACF ,sample PACF and use the ?L Jung Box Test to conclude the final model. The parameter estimation can be done based on the MLE/ Yule Walker equation/OLS approach. ARIMA models are fitted and accuracy of the model is tested on the basis of residual diagnostics. The L Jung Box test is applied on the residuals to determine whether they are white noise. The final time series model is thus ready for forecasting and prediction.

如果時間序列數據不穩定,則可以通過微分并再次執行ADF測試使其穩定。 重復此步驟,直到獲得穩定的時間序列。 在獲得沒有確定性趨勢的反季節平穩序列后,我們可以繼續進行模型識別。 該模型可以是AR(p)/ MA(q)/ ARMA(p,q)。 為了確定模型及其順序,我們計算了樣本ACF,樣本PACF并使用L Jung Box Test得出了最終模型。 可以基于MLE / Yule Walker方程/ OLS方法進行參數估計。 擬合ARIMA模型,并根據殘留診斷對模型的準確性進行測試。 將L Jung Box測試應用于殘差以確定它們是否為白噪聲。 因此,最終的時間序列模型已準備好進行預測和預測。

ILLUSTRATIONS1. Price forecast of paddy based on ARMA(1,1) model

插圖 1.基于ARMA(1,1)模型的稻谷價格預測

Based on the ACF and PACF correlogram, a time series ARIMA(1,1,1) model has been built to forecast paddy prices for the future.

基于ACF和PACF相關圖,建立了時間序列ARIMA(1,1,1)模型來預測未來的稻米價格。

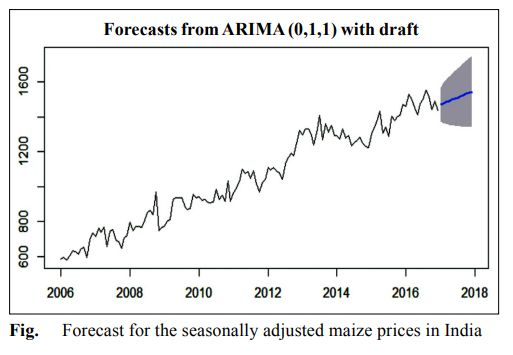

2. Price forecast of maize based on MA(1) model

2.基于MA(1)模型的玉米價格預測

3. Price forecast of pigeon pea based on AR(1) model

3.基于AR(1)模型的木豆價格預測

CONCLUSION

結論

The time series AR/MA/ARMA models serve as a good methodology for predicting the magnitude of any price variable. Its strength lies in the fact that the method is effective in any time series on agricultural prices with a pattern of change. Fluctuation in prices have increased significantly with a lot of uncertainty in profitability of growing agricultural crops. Under this scenario, forecasting future prices and disseminating the same to farmers to facilitate informed decisions by farmers before sowing is important. Forecasting of prices can help the farmers to decide the area allocation for a particular crop and marketing of agricultural produce. The forecasted values are almost similar to actual prices but like any other method, this technique also does not guarantee perfect forecasts. Nevertheless time series analysis is handy and can be successfully implemented using R and Python programming to get desired results.

時間序列AR / MA / ARMA模型可作為預測任何價格變量幅度的良好方法。 其優勢在于,該方法在任何時間序列上都可以有效地改變農產品價格。 價格的波動已經大大增加,而農業作物的獲利能力存在很多不確定性。 在這種情況下,預測未來的價格并將其分發給農民以促進農民在播種前做出明智的決定非常重要。 價格預測可以幫助農民確定特定作物的區域分配和農產品銷售。 預測值幾乎與實際價格相似,但是像其他任何方法一樣,此技術也不能保證完美的預測。 盡管如此,時間序列分析還是很方便的,并且可以使用R和Python編程成功實現,以獲得期望的結果。

REFERENCES1. V. Jadhav , B. V. Chinnappa Reddy , and G. M. Gaddi(2017), Application of ARIMA Model for Forecasting Agricultural Prices ,?J. Agr. Sci. Tech. Vol. 19: 981–9922. Ashwini Darekar · A. Amarender Reddy(2017),Price forecasting of maize in major states, ?Maize Journal 6(1&2): 1–53. Ashwini Darekar · A. Amarender Reddy(2017), Price forecasting of pulses: case of pigeonpea,?Journal of Food Legumes 30(3): 42–46

參考文獻 1. V. Jadhav,BV Chinnappa Reddy和GM Gaddi(2017),ARIMA模型在預測農產品價格中的應用,J。 農業 科學 科技 卷 19:981–9922。 Ashwini Darekar·A.Amarender Reddy(2017),主要州玉米價格預測,《玉米雜志》 6(1&2):1-53。 Ashwini Darekar·A.Amarender Reddy(2017),豆類價格預測:木豆案,《食品豆類雜志》 30(3):42–46

翻譯自: https://medium.com/analytics-vidhya/time-series-analysis-of-agricultural-prices-in-india-47e7ebebd8b4

為什么印度盛產碼農

本文來自互聯網用戶投稿,該文觀點僅代表作者本人,不代表本站立場。本站僅提供信息存儲空間服務,不擁有所有權,不承擔相關法律責任。 如若轉載,請注明出處:http://www.pswp.cn/news/391903.shtml 繁體地址,請注明出處:http://hk.pswp.cn/news/391903.shtml 英文地址,請注明出處:http://en.pswp.cn/news/391903.shtml

如若內容造成侵權/違法違規/事實不符,請聯系多彩編程網進行投訴反饋email:809451989@qq.com,一經查實,立即刪除!相關文章

SAP NetWeaver

)

NotifyMyFrontEnd 函數背后的數據緩沖區(一)

最后期限 軟件工程_如何在軟件開發的最后期限內實現和平

SQL Server的復合索引學習【轉載】

)

leetcode 1423. 可獲得的最大點數(滑動窗口)

pandas處理excel文件和csv文件

tukey檢測_回到數據分析的未來:Tukey真空度的整潔實現

spring— Spring與Web環境集成

Elasticsearch集群知識筆記

Item 14 In public classes, use accessor methods, not public fields

子集和與一個整數相等算法_背包問題的一個變體:如何解決Java中的分區相等子集和問題...

matplotlib圖表介紹

到2025年將保持不變的熱門流行技術

spring—SpringMVC的請求和響應

Maven+eclipse快速入門

馬爾科夫鏈蒙特卡洛_蒙特卡洛·馬可夫鏈

我如何在昌迪加爾大學中心組織Google Hash Code 2019

)