因果推斷(四)斷點回歸(RD)

在傳統的因果推斷方法中,有一種方法可以控制觀察到的混雜因素和未觀察到的混雜因素,這就是斷點回歸,因為它只需要觀察干預兩側的數據,是否存在明顯的斷點。

??注意:當然這個方法只能做到局部隨機,因此很難依據該結論推向全局。

本文參考自rdd官方示例,通過python的rdd包展示如何進行斷點回歸分析。

準備數據

# pip install rdd

import numpy as np

import pandas as pd

import matplotlib.pyplot as pltfrom rdd import rdd

# 設置隨機種子

np.random.seed(42)# 構造數據

N = 10000

x = np.random.normal(1, 1, N)

epsilon = np.random.normal(0, 1, N)

threshold = 1

treatment = np.where(x >= threshold, 1, 0)

w1 = np.random.normal(0, 1, N) # 控制變量1

w2 = np.random.normal(0, 4, N) # 控制變量2

y = .5 * treatment + 2 * x - .2 * w1 + 1 + epsilondata = pd.DataFrame({'y':y, 'x': x, 'w1':w1, 'w2':w2})

data.head()

| y | x | w1 | w2 | |

|---|---|---|---|---|

| 0 | 3.745276 | 1.496714 | 0.348286 | -7.922288 |

| 1 | 2.361307 | 0.861736 | 0.283324 | -4.219943 |

| 2 | 4.385300 | 1.647689 | -0.936520 | -2.348114 |

| 3 | 6.540561 | 2.523030 | 0.579584 | 0.598676 |

| 4 | 4.026888 | 0.765847 | -1.490083 | 4.096649 |

模型擬合

# 設置帶寬,只觀察斷點附近的數據表現

bandwidth_opt = rdd.optimal_bandwidth(data['y'], data['x'], cut=threshold)

print("Optimal bandwidth:", bandwidth_opt)

# 篩選帶寬內數據

data_rdd = rdd.truncated_data(data, 'x', bandwidth_opt, cut=threshold)

Optimal bandwidth: 0.7448859965965812

結果展示

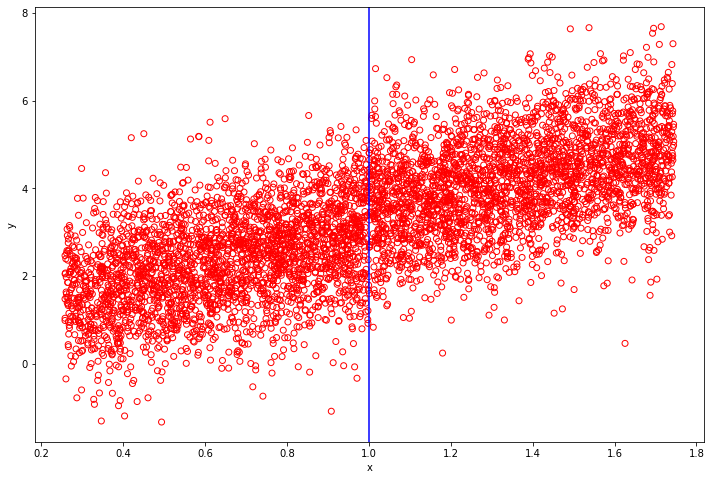

# 查看效果

plt.figure(figsize=(12, 8))

plt.scatter(data_rdd['x'], data_rdd['y'], facecolors='none', edgecolors='r')

plt.xlabel('x')

plt.ylabel('y')

plt.axvline(x=threshold, color='b')

plt.show()

plt.close()

# 數據混雜較多的噪音,對數據進行分箱,減少噪音

data_binned = rdd.bin_data(data_rdd, 'y', 'x', 100)plt.figure(figsize=(12, 8))

plt.scatter(data_binned['x'], data_binned['y'],s = data_binned['n_obs'], facecolors='none', edgecolors='r')

plt.axvline(x=threshold, color='b')

plt.xlabel('x')

plt.ylabel('y')

plt.show()

plt.close()

模型評估

# 查看模型效果

print('\n','{:*^80}'.format('model summary:'),'\n')

model = rdd.rdd(data_rdd, 'x', 'y', cut=threshold)

print(model.fit().summary())# 手動增加協變量,更改協方差類型

print('\n','{:*^80}'.format('model summary customize 1:'),'\n')

model = rdd.rdd(data_rdd, 'x', 'y', cut=threshold, controls=['w1', 'w2'])

print(model.fit(cov_type='hc1').summary())# 手動設置擬合方程

print('\n','{:*^80}'.format('model summary customize 2:'),'\n')

model = rdd.rdd(data_rdd, 'x', cut=threshold, equation='y ~ TREATED + x + w1*w2')

print(model.fit().summary())

*********************************model summary:********************************* Estimation Equation: y ~ TREATED + xWLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.508

Model: WLS Adj. R-squared: 0.508

Method: Least Squares F-statistic: 2811.

Date: Sun, 02 Oct 2022 Prob (F-statistic): 0.00

Time: 00:53:56 Log-Likelihood: -7794.0

No. Observations: 5442 AIC: 1.559e+04

Df Residuals: 5439 BIC: 1.561e+04

Df Model: 2

Covariance Type: nonrobust

==============================================================================coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 1.0297 0.046 22.267 0.000 0.939 1.120

TREATED 0.4629 0.054 8.636 0.000 0.358 0.568

x 1.9944 0.065 30.776 0.000 1.867 2.121

==============================================================================

Omnibus: 2.452 Durbin-Watson: 2.036

Prob(Omnibus): 0.293 Jarque-Bera (JB): 2.429

Skew: -0.034 Prob(JB): 0.297

Kurtosis: 3.077 Cond. No. 10.3

==============================================================================Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.***************************model summary customize 1:*************************** Estimation Equation: y ~ TREATED + x + w1 + w2WLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.523

Model: WLS Adj. R-squared: 0.523

Method: Least Squares F-statistic: 1520.

Date: Sun, 02 Oct 2022 Prob (F-statistic): 0.00

Time: 00:53:56 Log-Likelihood: -7709.9

No. Observations: 5442 AIC: 1.543e+04

Df Residuals: 5437 BIC: 1.546e+04

Df Model: 4

Covariance Type: hc1

==============================================================================coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 1.0297 0.045 22.797 0.000 0.941 1.118

TREATED 0.4783 0.054 8.870 0.000 0.373 0.584

x 1.9835 0.064 30.800 0.000 1.857 2.110

w1 -0.1748 0.014 -12.848 0.000 -0.201 -0.148

w2 0.0081 0.003 2.372 0.018 0.001 0.015

==============================================================================

Omnibus: 2.687 Durbin-Watson: 2.031

Prob(Omnibus): 0.261 Jarque-Bera (JB): 2.692

Skew: -0.032 Prob(JB): 0.260

Kurtosis: 3.088 Cond. No. 26.3

==============================================================================Notes:

[1] Standard Errors are heteroscedasticity robust (HC1)***************************model summary customize 2:*************************** Estimation Equation: y ~ TREATED + x + w1*w2WLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.523

Model: WLS Adj. R-squared: 0.523

Method: Least Squares F-statistic: 1194.

Date: Sun, 02 Oct 2022 Prob (F-statistic): 0.00

Time: 00:53:56 Log-Likelihood: -7709.6

No. Observations: 5442 AIC: 1.543e+04

Df Residuals: 5436 BIC: 1.547e+04

Df Model: 5

Covariance Type: nonrobust

==============================================================================coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 1.0303 0.046 22.617 0.000 0.941 1.120

TREATED 0.4784 0.053 9.054 0.000 0.375 0.582

x 1.9828 0.064 31.054 0.000 1.858 2.108

w1 -0.1746 0.014 -12.831 0.000 -0.201 -0.148

w2 0.0080 0.003 2.362 0.018 0.001 0.015

w1:w2 -0.0025 0.003 -0.737 0.461 -0.009 0.004

==============================================================================

Omnibus: 2.725 Durbin-Watson: 2.031

Prob(Omnibus): 0.256 Jarque-Bera (JB): 2.732

Skew: -0.033 Prob(JB): 0.255

Kurtosis: 3.088 Cond. No. 26.9

==============================================================================Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

上述模型表明TREATED有顯著影響

模型驗證

# 模型驗證

data_placebo = rdd.truncated_data(data, 'x', yname='y', cut=0) # 任意位置設置斷點

# 查看驗證效果

model = rdd.rdd(data_placebo, 'x', 'y', cut=0, controls=['w1'])

print(model.fit().summary())

Estimation Equation: y ~ TREATED + x + w1WLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.375

Model: WLS Adj. R-squared: 0.374

Method: Least Squares F-statistic: 660.8

Date: Sun, 02 Oct 2022 Prob (F-statistic): 0.00

Time: 00:53:56 Log-Likelihood: -4633.4

No. Observations: 3310 AIC: 9275.

Df Residuals: 3306 BIC: 9299.

Df Model: 3

Covariance Type: nonrobust

==============================================================================coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 1.0154 0.039 26.118 0.000 0.939 1.092

TREATED 0.0294 0.068 0.433 0.665 -0.104 0.163

x 1.9780 0.087 22.631 0.000 1.807 2.149

w1 -0.1752 0.017 -10.245 0.000 -0.209 -0.142

==============================================================================

Omnibus: 3.151 Durbin-Watson: 2.006

Prob(Omnibus): 0.207 Jarque-Bera (JB): 3.114

Skew: 0.057 Prob(JB): 0.211

Kurtosis: 3.098 Cond. No. 8.15

==============================================================================Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

隨機設置斷點在位置0,TREATED影響不顯著符合預期

總結

RDD能很好的針對政策干預、營銷活動的影響效果進行因果推斷。例如某平臺粉絲數達到10w會呈現大【V】標,我們就可以利用斷點回歸查看小于10萬附近的用戶收益和高于10萬用戶附近的用戶收益,是否存在明顯的斷點。

共勉~

)

)

)

)

)

)

| 筆記第1、2章)