張張張三豐de思考與總結:

最近做的期貨價格泡沫中,一直在說,momentum,momentum,momentum,那么究竟什么是momentum呢?

目前,在有關期貨價格泡沫的研究文獻中,一般都是研究較為宏觀的經濟變量對其影響,比如:經濟增長、利率、匯率、通貨膨脹等等,李劍老師的一些研究中,對宏觀因素已經做了較為完善的研究,甚至李劍老師還開發了綜合價格泡沫指標(好像是這一個詞的吧,好久了,記不太得了,好厲害,創新性buff加滿)

然而,關于中觀層面,甚至微觀層面的影響因素,很少很少有人研究,好像在2010-2020之間,有一個Masters 假說吧,是關于大宗商品指數投資的,經過好多好多學者驗證,其并不是期貨價格飆升的主要驅動力。以及研究投機等等的……對于交易所而言,宏觀層面不大可控,但是中觀和微觀層面還是可控的,了解其背后原因,對于價格的暴漲暴跌是有一定防控的,有利于維持價格穩定……

現在就從文獻中看看momentum是啥吧……

Large changes in stock prices: Market, liquidity, and momentum effect(2012)股價的巨大變化:市場、流動性和動量效應

摘要:本文研究了股票價格大幅變化的決定因素。經驗證據表明,在三個證券交易所中都發現了股票價格大變動的決定因素的不對稱現象。在紐約證券交易所(NYSE),動量效應是股價大幅上漲的主要可能性,而流動性特征則是股價大幅下跌的原因。一個有趣的發現是,在美國運通和納斯達克交易的股票則恰恰相反。對不同證券交易所不同結果的可能解釋可能歸因于在這些證券交易所上市公司的特點不同。

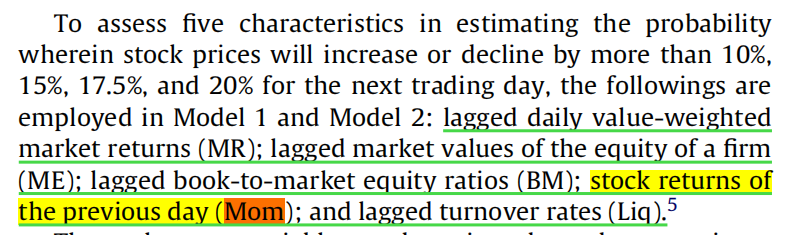

那么,是如何衡量動量效應的呢?動量效應又是是什么?以及流動性這些變量都是如何衡量的呢?

本文衡量Momentum使用的為:之前的股票回報(stock returns of the previous day)

we use five characteristics (one market-level and four firm-level variables), including market return(市場回報), size(規模), book-to-market ratio(賬面比), lagged returns(滯后回報), and turnover(周轉率),to explain large changes in stock returns(股價變動)

A new momentum measurement in the Chinese stock market(2022) 中國股市的一種新的動量指標

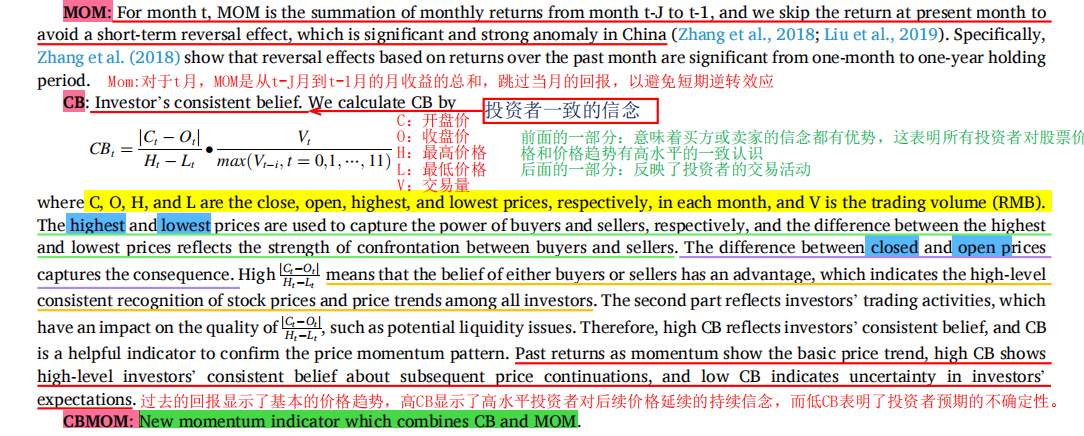

在許多國際市場和各種資產類別中都存在動量效應。然而,在包括中國在內的新興股票市場中,沒有傳統的momentum effect. (注:本文實證是構建了一個新的CBMOM的動量效應指標,結果發現:基于CBMOM的勢頭策略,一個月的CB和過去一年的回報率具有最強的利潤。the momentum strategy based on CBMOM with the one-month CB and the one-year past return has the strongest profit)

The momentum effect has been one of the widely studied anomalies. 動量效應是目前已被廣泛研究的異常現象之一。

Momentum theory believes that prices’ continuation is attributed to investors’ underreaction to information. 動量理論認為,價格的持續上漲要歸因于投資者對信息的反應不足。

News-watchers trade based on the advantages of private information, while momentum traders buy/sell shares based on price realized up? /down- trends (past returns). 新聞觀察者根據私人信息的優勢進行交易,而momentum交易者則根據價格實現的上漲的?/下跌趨勢(過去的回報)來買賣股票。

Intuitively, stock past performance is one of the sources for a momentum trader to form the buying or selling belief, and the shortterm information that can reflect other investors’ beliefs may be another decision-dependence source to the momentum trader.從直觀上看,股票過去的表現是動量交易者形成買賣信念的來源之一,而能夠反映其他投資者信念的短期信息可能是動量交易者的另一個決策依賴來源。

If momentum traders can conjecture other investors’ beliefs that are consistent with the price trend, they will be easier to execute a momentum strategy. Momentum traders who lack private information hope to achieve group advantage to alleviate concerns about potential price reversal or strengthen their momentum beliefs. 如果動量交易者能夠猜測其他投資者的信念與價格趨勢相一致,那么他們將更容易執行動量策略。缺乏私人信息的動量交易員希望獲得群體優勢,以緩解對潛在價格反轉的擔憂,或加強他們的動量信念。

momentum theory投資者對信息的反映不足……

根據過去的信息,形成買賣的行為

若momentum trader的行為和其他人一致,傾向于buy(羊群效應)

Momentum and Reversion to Fundamentals: Are They Captured by Subjective Expectations of House Prices?(2020)

主要借鑒文中的2個概念,momentum也是基于過去的房價Past momentum: △ P m , t △P_{m,t} △Pm,t?

Momentum refers that what was strongly increasing in the past will probably continue to increase in the near future.動量指過去強勁增長的東西在不久的將來可能會繼續增長。

Reversion to fundamentals refers that when asset prices have deviated from the long-run relationship with the fundamentals, there is a force driving those asset prices back to the long-run equilibrium level according to the fundamentals.回歸基本面指當資產價格偏離與基本面的長期關系時,有一股力量將這些資產價格根據基本面推回到長期均衡水平。

Pure momentum is priced(2019)純動量定價

Momentum is the strategy based on price continuation where investors buy (sell) stocks that have risen (declined) recently.動量是一種基于價格延續的策略,即投資者買入(賣出)最近已經上漲(下跌)的股票

M O M t MOM_t MOMt? is the momentum return in month t;

因研究的是基于Momentum定價,所以momentum是被解釋變量Y,但其定義也是價格的回報。與前面的都類似。

文心一言

Momentum是一種量化技術指標,用于衡量某只股票或期貨合約在某時間段內的價格變動幅度。

基于價格變動來計算,通過比較當前與一段時間前的價格差異來判斷市場的動量和趨勢,進而分析股價或期貨價格的強弱,預測未來的價格走勢。

Momentum指標在期貨市場中具有廣泛的應用價值,投資者可以根據其變化來判斷市場趨勢、確認買賣信號、判斷超買超賣狀態以及判斷市場波動性。然而,投資者在使用Momentum指標時需要注意其局限性,并結合其他技術指標和市場情況進行綜合分析,以降低投資風險。

然而,具體的衡量還應該參考文獻呀!

【三、MQ的核心類-消息類的存儲(用文件存儲消息)】? ★)

)

-附代碼)

)

useEffect、useRef、useImperativeHandle、useLayoutEffect)

)

)